AZZ’s Conglomerate Conundrum and the Avail Transformation

April 8, 2025

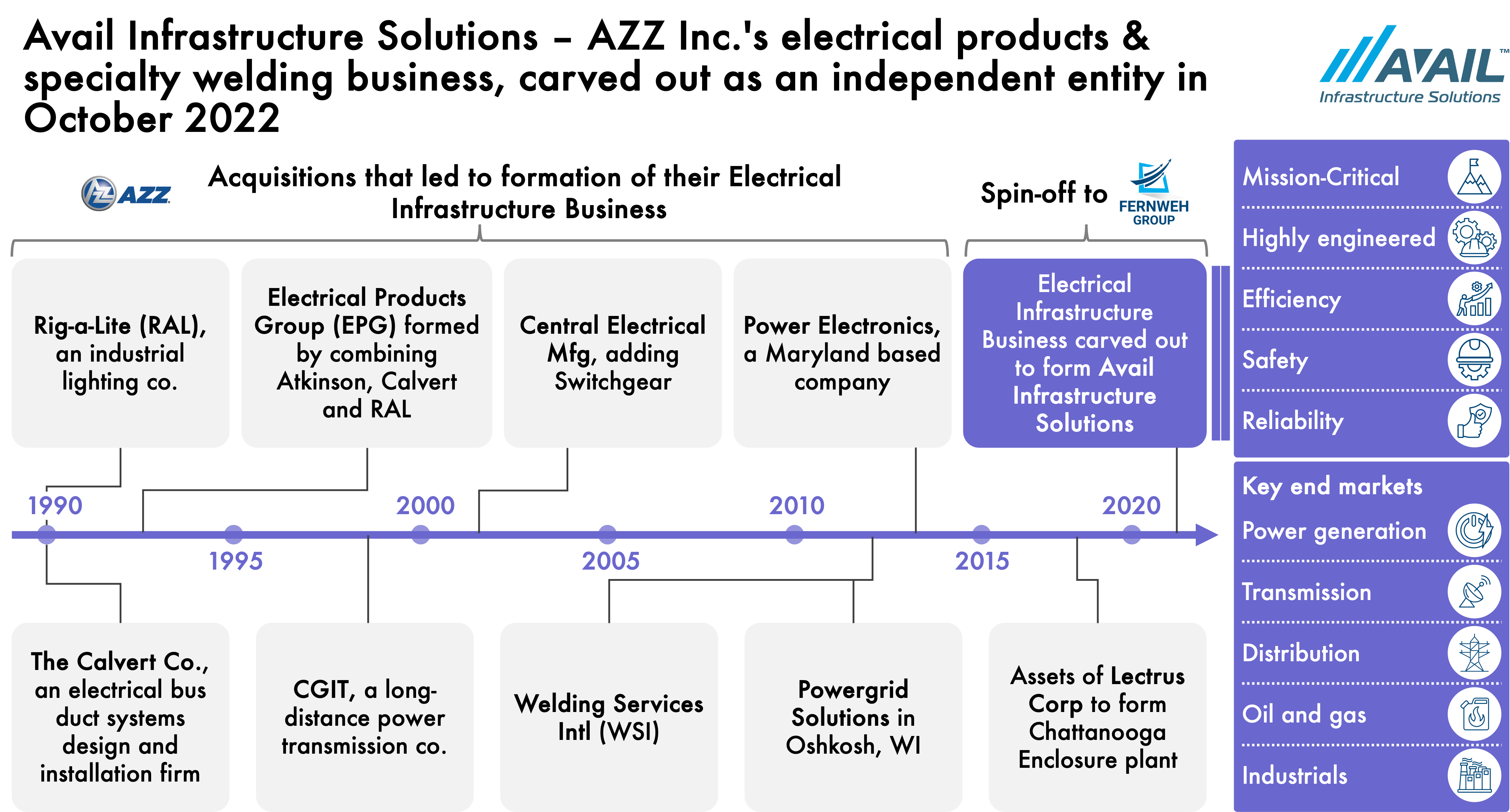

AZZ Inc., a long steady but underappreciated industrial player, spent two decades straddling distinct markets. Its business model paired a high-margin metal coatings division– anchored by cash-generating hot-dip galvanizing plants–with a diverse mix of electrical equipment and industrial services. The electrical segment grew through acquisitions like Rig-A-Lite1 and The Calvert Co.2 (1990), CGIT3 (1999). Also, added to the electrical equipment was the acquisition of Nuclear Logistics Inc4 in 2012. The industrial services arm expanded with Welding Services Inc., acquired as part of Aquilex SRO5 acquisition in Feb 2013. In November 2013, Tom Ferguson took over as CEO, steering the company into its next phase.

AZZ’s galvanizing segment follows a tolling model, offering corrosion protection to infrastructure and manufacturing customers, and has long delivered reliable free cash flow year after year. Analysts often acknowledged AZZ’s “rock-solid [multi-decade] record of turning a profit6,” yet the company’s stock remained stagnant (Exhibit 1), with investors largely indifferent despite strong margins (Exhibit 2) and 35+ years7 of profitability.

Exhibit 1

Exhibit 2

The challenge was perception—AZZ resembled a small conglomerate rather than a focused industrial leader. Its stable coatings business was paired with a more volatile infrastructure segment (later branded as AZZ Infrastructure Solutions), which produced switchgear, enclosures and specialty welding services. This mix left investors struggling to classify the company, preventing it from earning the valuation premium of a pure-play business or full recognition of its sum-of-the-parts value. Analysts were cautious about AZZ’s trajectory, noting that while its core metals business was solid, the infrastructure division remained a work in progress. A “conglomerate discount” masked AZZ’s true valuation.

AZZ’s board launched a strategic review in 2020 aimed at “accelerating the strategy to become a focused metal coatings company8”. This was a tacit admission that the status quo wasn’t working. The plan prioritized streamlining operations and shedding non-core units. AZZ quickly took action, divesting its NLI nuclear logistics unit9 and SMS field services10 in 2020. CEO Tom Ferguson, an operations veteran, recognized that AZZ’s valuation gap would persist unless the company sharpened its identity. Ferguson also realized that AZZ would need to expand its metal coatings business or risk becoming a sub-scale company. The stage was set for a bold move: splitting its galvanizing and electrical businesses to unlock their full potential.

Ferguson and his team began exploring options to spin off or divest the Infrastructure Solutions (AIS) segment. By early 2022, the rationale was clear – AIS, a diverse portfolio of electrical products (ranging from switchgear to lighting systems) and industrial services, had the potential to thrive outside of AZZ’s umbrella. Private equity players hesitated due to AIS’s mixed business lines, while strategic buyers faced complications—some AIS product lines overlapped with their own customers or competitors, making a full acquisition difficult.

With a straightforward sale presenting obstacles, AZZ took a creative approach. Instead of offloading AIS at a discount or spinning it off as a standalone entity without strategic backing, Ferguson orchestrated a partnership with Fernweh Group, an industrials-focused private investment firm founded by former McKinsey consultants Nick Santhanam, Shekhar Varanasi, and Siddarth Madhav.

In June 2022, AZZ finalized a carve-out agreement, structuring the deal to optimize both immediate cash proceeds and long-term upside. AZZ contributed AIS to a newly formed entity—later named Avail Infrastructure Solutions—and sold a 60% stake to Fernweh at a $300 million enterprise value, including $120 million of debt. This resulted in AZZ receiving ~$228 million in cash while retaining a 40% equity stake11. In essence, AZZ was cashing out a majority of AIS but keeping a foot in the door for the proverbial “second bite.” This structure allowed AZZ to monetize a majority of AIS while maintaining a foothold for future gains. “The agreement to divest a controlling stake in AIS…provides AZZ with near-term cash,” Ferguson noted, “but most importantly, it also allows us to participate in AIS’s value creation journey12.” The deal struck a careful balance of risk and reward—Fernweh assumed leadership of Avail and its transformation, but if the business flourished, AZZ’s shareholders would share in the upside. Ferguson had insisted on a structure that delivered a win-win scenario rather than a fire sale of an asset with untapped potential. Shareholders quickly recognized the value, commenting that the move allowed AZZ to focus on driving higher margins. Analysts also noted, “Historically, AZZ carried an adjusted EBITDA margin of ~15%. Through these transactions, AZZ projects a go-forward EBITDA margin closer to 20%. Q2 results validate this expectation13.”

A key driver of the carve-out’s potential was Fernweh’s operational expertise. Fernweh swiftly rebranded AIS as Avail Infrastructure Solutions, signaling a fresh strategic direction (Exhibit 3).

Exhibit 3

Fernweh, led by former McKinsey industrial experts, brought an “engaged investor & operator” playbook to Avail. Fernweh’s model combines sector-focused capital with hands-on operational expertise to “build businesses and create value” in mid-sized industrial tech companies. In Avail’s case, Fernweh deployed both its investment team and its affiliated operating partner, Ayna.AI, to drive the transformation. Ayna specializes in performance improvement for industrial companies – it “combines domain expertise, transformation capabilities, and an engaged operator model” to create standout performers. Shortly after acquisition, Fernweh and Ayna worked closely with AIS leadership to identify quick wins and longer-term improvements. They established rigorous performance metrics and a “keep score” mentality, leveraging Ayna’s data-driven tools for granular visibility into operations (from plant-level efficiency to working capital management). Fernweh’s team also brought industrial process improvement expertise and fresh strategic perspectives, which AZZ’s CEO acknowledged would bode well for Avail’s future.

Crucially, Fernweh wasted no time in restructuring Avail’s leadership to execute the turnaround. The firm tapped proven operators to steer the standalone business. In October 2022, mere days after closing, Fernweh installed William “Bill” Johnson – an industry veteran – as CEO of Avail14. Johnson’s pedigree was ideal for an industrial carve-out: he had led multiple manufacturing companies and recently grew Welbilt Inc. to $1.7 billion in revenue with ~20% EBITDA margins, culminating in its $4.8 billion sale in mid-202215. Alongside Johnson, Fernweh brought in Marty Agard as CFO and Jen Gudenkauf as CHRO – both fellow alumni of Welbilt – to form a new top team16. This influx of external talent was paired with continuity from AIS’s ranks: Fernweh retained and promoted AZZ veterans Jeremy Hoffman as Avail Electrical Product Group (EPG)’s President & COO and Bill Ruta as Vice President of WSI17. By blending insiders who knew the legacy business with outsiders adept at transformation, Fernweh set up a leadership dynamic geared toward change but mindful of core strengths.

Under the new leadership, Avail underwent a cultural and operational overhaul. Bill Johnson quickly articulated a vision to make Avail the “partner of choice” in its industry, emphasizing quality, innovation, and customer service. Early operational changes focused on efficiency and integration: Avail streamlined its manufacturing footprint and optimized its product lines. The company had inherited a broad portfolio – from custom switchgear and electrical enclosures to medium/high-voltage bus ducts and explosion-proof lighting. Johnson’s team reviewed this portfolio to refocus on higher-margin, “application-critical” offerings. They invested in lean manufacturing practices at Avail’s 10+ facilities and implemented standardized KPIs across formerly siloed business units (bus systems, switchgear, enclosures, lighting, and the WSI welding services unit).

A key move was breaking down the AIS segment’s sub-divisions into more cohesive groups under new general managers, each accountable for profitability. Avail’s org chart now featured dedicated GMs for Bus Systems, Switchgear Systems, Enclosure Systems, etc., reporting to a dynamic COO and EPG leader (Hoffman). This structure, along with Ayna’s on-the-ground support, enabled faster decision-making and cross-selling among product lines (for instance, bundling switchgear and bus duct solutions in turnkey projects). Operational processes were also digitized – Ayna helped implement better ERP analytics and demand forecasting tools, reducing lead times and inventory levels. By introducing financial transparency and accountability at all levels, Johnson’s team created a performance-oriented culture. Avail employees, many of whom had been part of a slow-moving corporate segment, now had equity incentives and a startup-like mandate to “build” the business. The new owners’ engaged approach was a marked shift from the conglomerate era, and it resonated: “the combination of Fernweh’s management and Avail’s brand” motivated teams to meet growing market needs.

Strategically, Avail pivoted to capture emerging opportunities in the electrical infrastructure arena. Under Fernweh’s ownership, Avail has placed greater emphasis on fast-growing end markets – notably data centers, renewable energy, and electric vehicle (EV) charging infrastructure. The legacy AIS business had strong positions in traditional power generation and industrial markets; Fernweh saw chance to extend into new segments riding secular growth trends. For example, in September 2024 Avail acquired WASP Critical Power & Equipment Solutions (CPES)18, a specialist in low-voltage switchgear for data centers and EV infrastructure. “Combining CPES’s capabilities with Avail’s management and infrastructure will allow us to meet growing market needs,” noted CPES’s president19, highlighting Avail’s commitment to these expanding sectors. Earlier, in May 2023, Avail had also purchased critical assets of Custom Power Enclosures (CPE)20 to scale up its custom electrical enclosure production. These tuck-in acquisitions, orchestrated by Fernweh, filled product gaps and boosted Avail’s ability to offer integrated solutions (from enclosures and switchboards to bus ducts and on-site services). In tandem, Avail’s RIG-A-LITE lighting unit launched new hazardous-duty LED products for niche markets (like food processing), and the WSI services unit inked international partnerships (e.g. with Kanoo Energy in the Middle East). Such moves broadened Avail’s reach and positioned it squarely in the heart of the industrial electrification wave – aligning the company with the infrastructure upgrade cycle and energy transition initiatives in the broader economy.

This carve-out was far more than a financial transaction—it was a full-scale operational reboot for AIS, now under new ownership yet with AZZ retaining a strategic minority stake

AZZ saw immediate benefits from the carve-out. By 2023, it had transformed into a more focused enterprise centered on its Metal Coatings segment and a new crown jewel: the Precoat Metals coil-coating unit (acquired in May 2022 for $1.3 billion21). AZZ financed the transaction with a mix of debt and equity-linked securities, including $240 million in 8-year Subordinated Convertible Notes purchased by Blackstone22.

While hot-dip galvanizing and coil coating may not capture mainstream attention, they are stable, high-margin businesses with steady demand. Investors began viewing AZZ in a new light— “predominantly a metal coatings company,” as Ferguson had envisioned. The complexity and cyclicality of AIS were no longer weighing on its valuation. AZZ could now be assessed purely on the strength of its coatings businesses, which held leading market positions. “[AZZ] is the leading independent provider of hot dip galvanizing and coil coating solutions in North America,23” the company noted, finally able to present a clear and compelling narrative. With the conglomerate discount lifted, AZZ started receiving long-overdue recognition.

Beyond optimizing its portfolio, the carve-out also delivered immediate financial and operational benefits of a deconsolidation to AZZ. Retaining a 40% minority stake in Avail allowed AZZ to participate in future value creation while removing the need for full financial disclosures of the business. This not only simplified AZZ’s income statement and balance sheet but also improved transparency for investors, reinforcing its identity as a streamlined, high-margin metal coatings company.

Since Avail’s carve-out, AZZ’s core coatings businesses have thrived. By concentrating on galvanizing plants and coil coating lines, the company capitalized on rising infrastructure spending and manufacturing reshoring, even outperforming larger peers. Its bold Precoat acquisition began to pay off as demand for pre-painted steel surged. As financial performance strengthened, the stock market took notice. After languishing in the mid-$30s in 2020, AZZ shares climbed steadily following the Avail deal and strategic refocus. By the end of 2023, the stock had nearly doubled from its 2022 trough and surged another 43% in 2024 alone (Exhibit 4). Analysts, who had once overlooked AZZ, initiated coverage with bullish outlooks. Roth MKM praised the company’s “steady” organic growth, operational efficiencies, and expanding free cash flow24, projecting 4–5% annual organic growth for the streamlined business.

Exhibit 4

In short, AZZ’s bet on specialization paid off, delivering the clarity and valuation uplift shareholders had long sought. With a cleaner profile and strong execution, the company even achieved higher earnings multiple, closing the gap with peers and validating Ferguson’s breakup strategy. Analysts were enthusiastic about management’s execution, noting both top- and bottom-line improvements alongside a rising stock price. The company received major upgrades as investors recognized its ability to “capitalize on secular growth trends, such as the reshoring of manufacturing to the US and increased use of aluminum and pre-painted steel25.”

If AZZ’s progress was impressive, Avail’s transformation was even more striking. Under Fernweh’s ownership, Avail Infrastructure Solutions embarked on an ambitious turnaround—Spark Program (Exhibit 5) in collaboration with Ayna. Through this program, the Ayna team partnered with Bill Johnson, Marty Agard, and rest of the Avail leadership team to swiftly address inefficiencies and operational silos that had previously constrained AIS. They optimized plant operations, streamlined product lines, and accelerated the shift toward higher-margin segments, such as custom-engineered enclosures for data centers and grid infrastructure.

Exhibit 5

In under two years, Avail’s EBITDA is set to nearly triple from ~$37 million in 2021/22 to nearly $100 million by 2025—an extraordinary turnaround for what was once AZZ’s underperforming unit. Revenues are on track to increase by 1.6× from the ~$375 million at carve-out, with EBITDA margins expanding by an estimated 630 basis points (Exhibit 6), nearing those of much larger industrial peers. “We have commenced the transformation of Avail… building on a strong financial base to drive growth26,” noted Fernweh CEO Nick Santhanam at closing, confident in Avail’s trajectory. The company has even pursued bolt-on acquisitions, including a Texas manufacturing facility, to meet rising utility sector demand. Once a fragmented business, Avail is now a focused platform capitalizing on booming markets like power grid modernization and data infrastructure.

Exhibit 6

As an independent entity, Avail has carved out a unique niche in a competitive market (Eaton, ABB, Schneider Electric)—agile enough for custom solutions yet broad enough for large-scale needs. This “segment-of-one” positioning aligns with Fernweh’s engaged operator strategy, mirroring how PE firms capitalize on conglomerates streamlining portfolios to create focused growth platforms. Avail’s rebranding coincided with the U.S. manufacturing resurgence, benefiting from reshoring trends and renewed investor interest in industrials.

Avail’s focus on electrical infrastructure aligns with critical economic priorities—grid reliability, data sovereignty, and energy transition—further underscoring its strategic importance. AZZ’s filings highlight Avail’s rapid financial ascent: equity income from its 40% stake jumped from $2.6 million27 (partial 2023) to a projected $15–18 million in fiscal 202528, implying Avail’s net income run rate has surged to ~$40–45 million. Revenues are set to surpass $600 million in 2025 (vs. $375M in 2022), fueled by double-digit organic growth and acquisitions. CEO Nick Santhanam lauded “the company’s strong financial performance” from the outset, and results have validated that confidence. By relentlessly executing—shortening production cycles, reducing overhead, and expanding sales reach—Avail has markedly improved efficiency. Working capital turns improved, and EBITDA-to-cash conversion remained strong despite growth, signaling disciplined financial management.

For AZZ shareholders, the carve-out and co-ownership of Avail proved a financially astute move. A full sale of AIS in 2022 might have yielded $300 million in pre-tax cash, but by structuring a joint venture, AZZ secured an upfront infusion ($230 million) while retaining a 40% stake in Avail’s upside. This illustrates the genius of the “have your cake and eat it” approach: initial proceeds near $230 million plus a minority interest now plausibly worth many times that. Little wonder that AZZ’s management calls the carve-out a “win-win”. “We believe the successful execution of our strategic plans will build momentum and drive sustainable value creation for all of our stakeholders.29” Ferguson had said during the process – a statement that now reads as plain fact.

The structure also aligned incentives seamlessly. With majority control, Fernweh was motivated to drive Avail’s growth, while AZZ, as a large minority shareholder, stood to benefit. Employees also gained, shifting to a more entrepreneurial, sector-focused company.

Indeed, in March 2025, Fernweh’s announced sale of Avail’s EPG BU to nVent PLC for $975 million underscored the transformation’s success—more than 3× its initial $300M enterprise value. This transaction validates the power of strategic carve-outs, turning a "non-core" asset into a high-value, standalone firm. Avail story thus serves as a playbook for executing carve-outs in the industrial sector, combining smart deal structuring, savvy operational leadership, and strategic capital deployment to deliver superior outcomes. It validates Fernweh’s thesis that applying private equity and consulting rigor to under-optimized industrial assets can unlock “alpha” returns.

Ferguson has orchestrated a carve-out that stands as a case study in thoughtful corporate restructuring. Rather than a messy conglomerate breakup or a zero-sum sale, AZZ and Fernweh crafted a partnership to rejuvenate a business and reward all parties. AZZ’s stockholders saw their company shed its conglomerate discount and surge in value. Fernweh obtained a platform (Avail) to build into a major player in electrical infrastructure – and by all accounts, that bet is paying off handsomely. And AZZ maintained a lucrative slice of that success while refocusing on its core competency in coatings. In the end, what began as a response to investor agitation became a story of value creation. A once incongruous collection of assets has been split into two thriving enterprises. AZZ found a way to avail itself of an opportunity to galvanize shareholder returns – turning an old-school breakup into a modern win-win deal for the “Titanium Economy” age.

Avail’s transformation story is emblematic of a broader opportunity in the U.S. industrial and manufacturing sector. Many mid-sized industrial technology businesses – often hidden inside conglomerates – have the potential for outsized performance once given focus and resources. Fernweh’s founders have dubbed this class of companies the “Titanium Economy,” highlighting their strength and resilience. These firms, frequently overlooked by Wall Street, form the “backbone of the economy and the engine for its growth,” as Fernweh puts it. Avail fits this description well: it produces unglamorous but mission-critical equipment (electrical bus ducts, switchgear, welding solutions) that keeps power plants, data centers, and factories running safely. In recent years, such industrial tech providers have enjoyed robust tailwinds. Aging electrical infrastructure in North America, the boom in cloud computing data centers, and the push for electrification (EV charging networks, renewable integration) all drive demand for Avail’s products. The U.S. Bipartisan Infrastructure Law and other initiatives are spurring billions in grid upgrades – benefitting suppliers like Avail that offer solutions from “medium and high voltage bus systems” to turnkey electrical enclosures.

Transformations of this nature are never easy. Success requires rigorous commitment from all stakeholders—AZZ, Fernweh, Avail, and Ayna. For the operating partner, Ayna’s ability to swiftly identify winning strategies while maintaining focus on long-term transformation goals was critical in maximizing value creation. A shared sense of confidence and urgency in executing the M&A strategy was essential, particularly as Avail needed to quickly gain market share in emerging sectors like data centers and EVs. As a carveout competing against large industrial players, Avail was an underdog. However, its experienced executive leadership—comprising transformation and EPG experts from AZZ and Avail, alongside Fernweh/Ayna’s seasoned professionals in strategy and industrial value creation—played a pivotal role in driving its success.

Ayna, in collaboration with Avail’s leadership, spearheaded targeted initiatives under the SPARK program to enhance financial and operational performance. Stringent cash management strategies reduced net working capital to below 20% of revenue, while disciplined customer collections improved liquidity. Inflation was proactively managed by establishing index pricing for material expenditures and optimizing pricing levers to protect margins. Strategic acquisitions, including CPE in Houston and Wasp Critical Power Solutions, expanded Avail’s capacity and expertise in key markets. Additionally, product innovations—such as eco-friendly gas-insulated bus systems and high-capacity DC bus systems for hydrogen applications—demonstrated Avail’s commitment to evolving industry demands.

The partnership between Fernweh and AZZ was built on a foundation of mutual trust and a shared vision. Both firms took bold steps in brokering the AIS deal: AZZ recognized the shifting landscape of its infrastructure segment and, against traditional practice, opted for a JV structure that prioritized long-term value over immediate cash. Meanwhile, Fernweh/Ayna took on a historically underperforming business in a competitive market—an ambitious move for an early-stage PE firm. This trust-driven partnership was rooted in the belief that win-win solutions are possible and that the industrial sector is filled with untapped potential. Fernweh’s engaged investor-operator model successfully strengthened relationships, scaled teams, and propelled Avail to new heights in the EPG market—culminating in its integration into nVent, where it is now poised to add significant value.

This transformation would not have been possible without Avail’s exceptional leadership team. CEO William Johnson brings extensive experience from his tenure as CEO of Welbilt and leadership roles at Chart Industries, Dover Corporation, Hillphoenix, Triton Systems, and Graham Corp. CFO Martin D. Agard provides deep financial expertise from his time as CFO at Lumber Liquidators and prior finance roles at Kohler Co., Georgia – Pacific, and HomeBanc Mortgage Corp. CHRO Jen Gudenkauf offers critical human resources insights from her roles as Executive Vice President and Chief Human Resources Officer at Welbilt, Vice President of Human Resources – North America at Sykes Enterprises, and various HR leadership positions at Bloomin’ Brands, OSI Restaurant Partners, and Gentiva Health Services. Their collective expertise has been instrumental in driving Avail’s sustained growth and innovation.

1 "HistoricalTimeline," AZZ Inc., accessed March 17, 2025,https://www.azz.com/historical-timeline/.

2 Ibid.

3 Ibid.

4"AZZ IncorporatedSigns Agreement to Acquire Nuclear Logistics Inc.," PR Newswire,April 30, 2012,https://www.prnewswire.com/news-releases/azz-incorporated-signs-agreement-to-acquire-nuclear-logistics-inc-149458875.html.

5 "AZZ IncorporatedCompletes Acquisition of Aquilex Specialty Repair and Overhaul LLC," PRNewswire, April 1, 2013,https://www.prnewswire.com/news-releases/azz-incorporated-completes-acquisition-of-aquilex-specialty-repair-and-overhaul-llc-200896611.html.

6 Investing, Kenyo."AZZ Inc.: Here's What A Real Moat Looks Like." Seeking Alpha,December 22, 2015.https://seekingalpha.com/article/3772066-azz-inc-heres-what-a-real-moat-looks-like.

7 AZZ Inc., 2024 AnnualReport (Fort Worth, TX: AZZ Inc., April 22, 2024), Page 2,https://www.azz.com/wp-content/uploads/2024/05/AZZ-Inc-2024-Annual-Report-Web-Ready-5-22-24.pdf.

8 AZZ Inc., 2023 Annual Report (Fort Worth,TX: AZZ Inc., May 2023), 2,https://www.azz.com/wp-content/uploads/2023/05/23-14919-1_470046_AZZ-Annual-Report-Web-Ready.pdf.

9 "AZZ Inc. Announces theDivestiture of its Nuclear Logistics LLC Operating Business to Paragon Energy Solutions,"PR Newswire, February 11, 2020,https://www.prnewswire.com/news-releases/azz-inc-announces-the-divestiture-of-its-nuclear-logistics-llc-operating-business-to-paragon-energy-solutions-301002470.html

10 "AZZ Inc. Announces theDivestiture of the AZZ SMS LLC Business," PR Newswire, October 26, 2020,https://www.prnewswire.com/news-releases/azz-inc-announces-the-divestiture-of-the-azz-sms-llc-business-301159869.html

11 "AZZ Inc. Enters Definitive Agreement toDivest Majority Interest in the Company's Infrastructure SolutionsSegment," PR Newswire, June 23, 2022, https://www.prnewswire.com/news-releases/azz-inc-enters-definitive-agreement-to-divest-majority-interest-in-the-companys-infrastructure-solutions-segment-301574467.html.

12 Ibid.

13 Steinmetz, Anthony H. "AZZ Inc: Transformation OnTrack Despite Market Reaction To Q2 Earnings." Seeking Alpha,November 9, 2022.https://seekingalpha.com/article/4555293-azz-inc-transformation-on-track-despite-market-reaction-to-q2-earnings.

14 Fernweh Acquires MajorityStake in AZZ’s Infrastructure Solutions Segment and Rebrands as AvailInfrastructure Solutions, MyNewsDesk, October 3, 2022, https://www.mynewsdesk.com/dabico-airport-solutions/pressreleases/fernweh-acquires-majority-stake-in-azzs-infrastructure-solutions-segment-and-rebrands-as-avail-infrastructure-solutions-3208432.

15 Ali Group and WelbiltAnnounce Definitive Merger Agreement, Business Wire, July 14, 2021, https://www.businesswire.com/news/home/20210714005699/en/Ali-Group-and-Welbilt-Announce-Definitive-Merger-Agreement.

16 Fernweh Acquires MajorityStake in AZZ’s Infrastructure Solutions, MyNewsDesk, October 3, 2022.

17 Company Leadership, Avail InfrastructureSolutions, accessed March 11, 2025,https://www.availinfra.com/company-leadership/.

18 Critical Power EquipmentSolutions, Avail Infrastructure Solutions, September 24, 2024,https://www.availinfra.com/press_release/critical-power-equipment-solutions/.

19 Ibid.

20 CPE Houston, AvailInfrastructure Solutions, May 23, 2023, https://www.availinfra.com/press_release/cpe-houston/.

21 "AZZ Inc. Completes Acquisition of Precoat Metals fromSequa Corporation," PR Newswire, May 13, 2022,https://www.prnewswire.com/news-releases/azz-inc-completes-acquisition-of-precoat-metals-from-sequa-corporation-301546948.html.

22 "AZZInc. Announces Financing of Precoat Transaction," PR Newswire,April 25, 2022, https://www.prnewswire.com/news-releases/azz-inc-announces-financing-of-precoat-transaction-301532271.html.

23 AZZ Inc., "InvestorRelations," AZZ Inc., accessed March 10, 2025,https://www.azz.com/investor-relations/.

24 "AZZ Inc. Initiatedwith a Buy at Roth MKM", Business Insider, February 11, 2025,https://markets.businessinsider.com/news/stocks/azz-inc-initiated-with-a-buy-at-roth-mkm-1034340313.

25 Insights, RL. "AZZ:Balanced Outlook With Growth In Infrastructure, Softness In PrivateSector." Seeking Alpha, October 29, 2024. https://seekingalpha.com/article/4730272-azz-balanced-outlook-with-growth-in-infrastructure-softness-in-private-sector.

26 "Fernweh AcquiresMajority Stake in AZZ Infrastructure Solutions Segment and Rebrands as AvailInfrastructure Solutions," Fernweh Group, October 3, 2022,https://www.fernweh.com/fernweh-news/fernweh-acquires-majority-stake-in-azz-infrastructure-solutions-segment-and-rebrands-as-avail-infrastructure-solutions.

27 AZZ Inc., FY2023 Q4 andFull-Year Earnings Deck, April 25, 2023,https://www.azz.com/wp-content/uploads/2023/04/Earnings-Deck-FY2023-Q4-and-Full-year-042523-7.30AM_FINAL.pdf.

28 AZZ Inc., Q3 FY25 Earnings Release,January 2025,https://www.azz.com/wp-content/uploads/2025/01/Exhibit-99.1-Q3-FY25-Earnings-Release-FINAL.pdf.

29 AZZ Inc. (AZZ) Q2 2024Earnings Call Transcript," Seeking Alpha, October 11, 2023,https://seekingalpha.com/article/4640240-azz-inc-azz-q2-2024-earnings-call-transcript.

This article explores what some industrial manufacturing companies are doing differently, and how others can close the gap between digital and AI potential and payoff.

This article explores what some industrial manufacturing companies are doing differently, and how others can close the gap between digital and AI potential and payoff.

Subscribe to the The Titanium Economy newsletter to read the article.

Subscribe to get the latest news from The Titanium Economy.

.jpg)